What Is a 401k Plan and how does it work?

How does a 401k work? Many of us have 401k plans through our place work work so this is a fairly common questions. Before we get into it, let’s talk about retirement savings.

Everyone should be saving for retirement. However, most American’s won’t retire with enough money in the bank to sustain themselves. 64% of Americans are now expected to retire with less than $10,000 in the bank according to a 2019 retirement survey by GoBankingRanks. Despite this small sum which likely wouldn’t carry most Americans through half a year of living expenses, nearly half of respondents were not concerned. Less than 17% will retire with more than $100,000 in the bank. Top reasons for not saving enough included not making enough money and paying down debt.

For those in their 20s and 30s, saving for retirement may not seem like a priority. However, small investments today, will yield high returns in the future.

Before we dive into the specifics, picture this. You’re 25 years old making $40,000. Your employer has a 401k plan and they claim they will “match” your contribution up to 5%. Sound good…but what does this mean? The 401k is one of the most common retirement plans offered today. It’s an easy way to set yourself up for a nice retirement account. But what is it and how does a 401k work?

What is a 401k and How Does it Work?

A 401k is a retirement plan sponsored by your employer. This plan allows employees to invest a portion of their income tax-free into an investment portfolio. 401ks are great for a few reasons:

- Taxes are only taken out after the money is withdrawn so employees are able to invest a larger sum upfront.

- Many employers will match funds meaning that they will invest additional funds from their own account up to a specific percentage.

- 401ks allow the employee to invest how they choose-typically most plans offer a spread of mutual funds, stocks, bonds, and other investments. Over time employees can change investment portfolios depending on their life stage (being more conservative as one ages).

What Are Some of the Restrictions?

While the 401k is a great way to set aside funds for retirement, there are some restrictions.

- Employer matched contributions sometimes don’t kick in until you’ve been vested for a specific amount of time (your own contributions are effective immediately).

- There are rules about when you can withdraw your funds. If you withdraw early you risk paying the 10% early withdrawal fee.

- The IRS will cap how much you can contribute every year. It was just announced in November of 2021, that the 2022 employee contribution limit will increase from $19,500 to $20,500, meaning Americans will soon be able to set aside even more for retirement. However, according to the IRS website, employer contributions remain the same at $58,000. If you are 50+, you are allotted an additional “catch up” contribution of $6,500 (this still remains the same for 2022). (1)

When Can I Access this Money?

You can start to take out funds at age 59 ½ without any penalties. There are no withdrawal requirements at this age but you are required to withdraw the minimum amount by at least age 72.

You can access your funds earlier than 59 ½ penalty-free for hardships if you qualify but you will still owe taxes.

How Much Money Can I Really Save with a 401k?

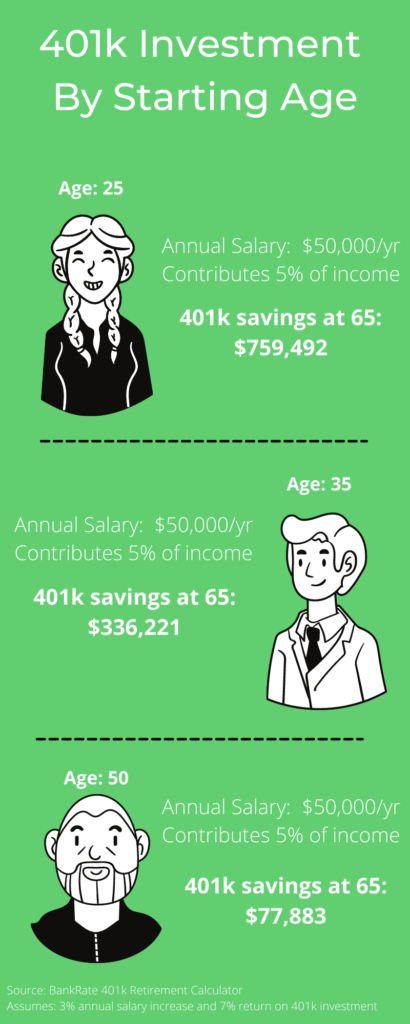

Below we have an infographic that illustrates a very important point: Invest Early.

To bring this to life, consider the following parameters:

You are investing 5% of your salary every year from age 25-65 with an annual salary of $50,000 and a projected +3% annual increase. Your portfolio will yield an average annual return of +7%.

If you start investing at age 25, at retirement you’ll net over $750k! However, if you wait till you’re 35 to start investing, you will end up losing out on $400k!!! Start at 50 and you can basically kiss a six figure retirement portfolio good-bye. Note that these figures are based on specific inputs noted above and will vary with your individual situation. The point however, is that investing early, even a nominal amount like 5% will make a tremendous difference because of compound interest.

Far better than the $10,000 most Americans will have right?

For more information check out the IRS website.

For additional retirement savings ideas check out the investment section of our website.

Sources:

(1) Retirement Topics-401(k) and Profit Sharing Plan Contribution Limits. https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-401k-and-profit-sharing-plan-contribution-limits Accessed March 2, 2021